library(lavaan)

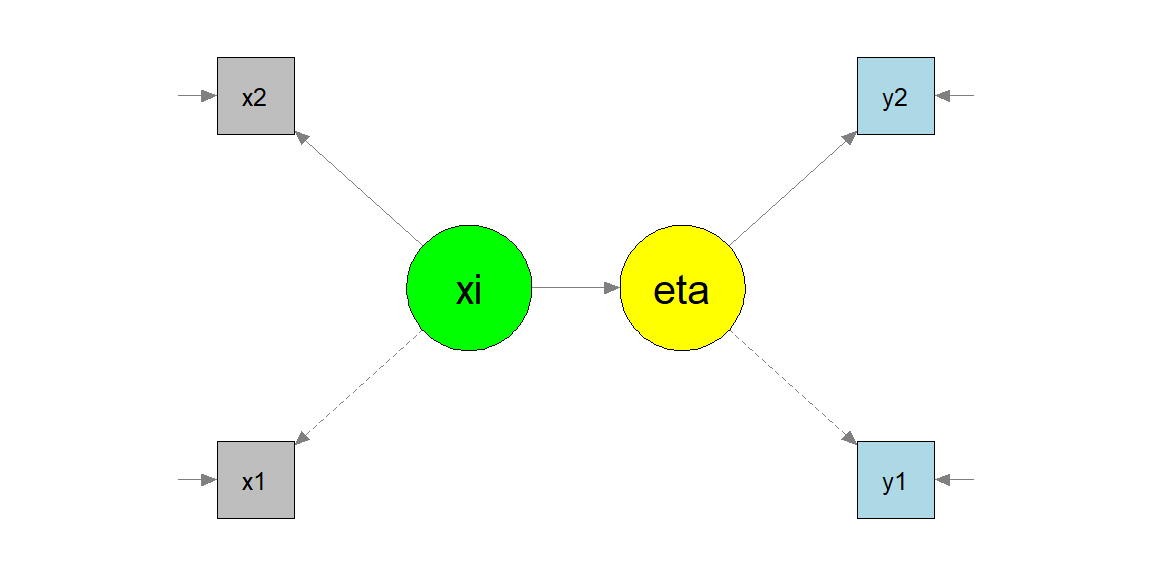

dSEM <- simulateData("xi =~ .74*x1 + .65*x2 # note the =~

eta =~ .56*y1 + .75*y2

eta ~ .30*xi # and the ~ only

", sample.nobs = 1000)Structural Equation Models

Measurement + structure (capstone)

Tommaso Feraco

Today in the workflow

Specify → Identify → Estimate → Evaluate → Revise/Report

Today: full SEM = measurement model (CFA) + structural model (paths among latent variables).

We will repeat fit/diagnostics on purpose: by now it should become a habit (global + local).

Learning objectives

By the end of this session you should be able to:

- Connect the CFA measurement model to the SEM structural model (two-step mindset)

- Understand how SEM is represented in matrices (\(Λ\), \(B\), \(Γ\), \(Φ\), \(Ψ\), \(Θ\))

- Fit a full SEM in lavaan and interpret parameters + fit indices + diagnostics

- Compare plausible SEMs (nested comparisons) and justify modifications transparently

Structural equation models

Up to now, we have seen how to model the relationship between different variables/constructs at the same time (path analysis) and how to build a measurement model with one or more latent variables.

A complete SEM takes both of these things and put them together.

The two parts of a SEM

The measurement model

\(x = \Lambda_x\xi + \delta\)

\(y = \Lambda_y\eta + \epsilon\)

The structural model

- \(\eta = B\eta + \Gamma\xi + \zeta\)

already seen in the first slides

Matrices

These models (can) have all the possible matrices:

Loadings and coefficients matrices

- \(\Lambda^x\) - relation among \(\xi\) and \(x\)

- \(\Lambda^y\) - relation among \(\eta\) and \(y\)

- \(B\) - relation among \(\eta\) and \(\eta\)

- \(\Gamma\) - relation among \(\xi\) and \(\eta\)

Covariance matrices

- \(\Theta^\delta\) - \(x\) errors

- \(\Theta^\epsilon\) - \(y\) errors

- \(\Psi\) - \(\eta\) errors

- \(\Phi\) - relations among \(\eta\)

Different models are allowed based on the way we define relationships among variables

… lavaan matrices

lavaan does not distinguish between endogenous and exogenous variables. This leads to an easier parametrization and to four matrices only:

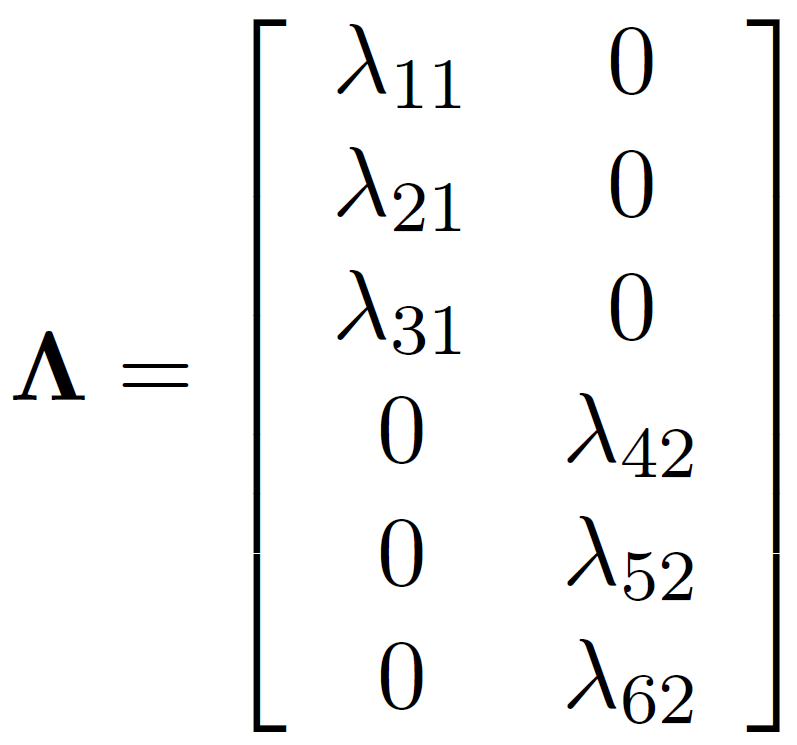

- \(\Lambda\) factor loadings matrix \([p x m]\)

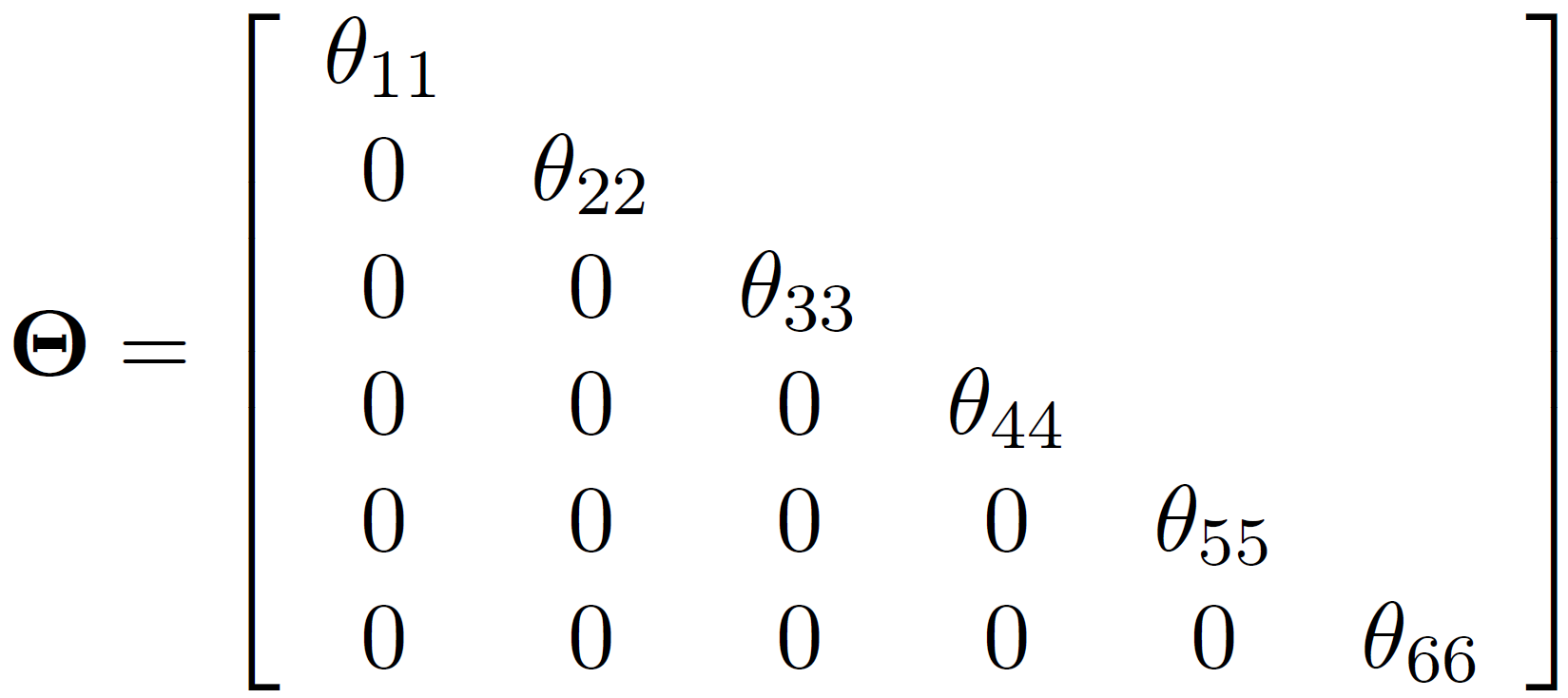

- \(\Theta\) measurement residual errors covariance matrix \([p x p]\)

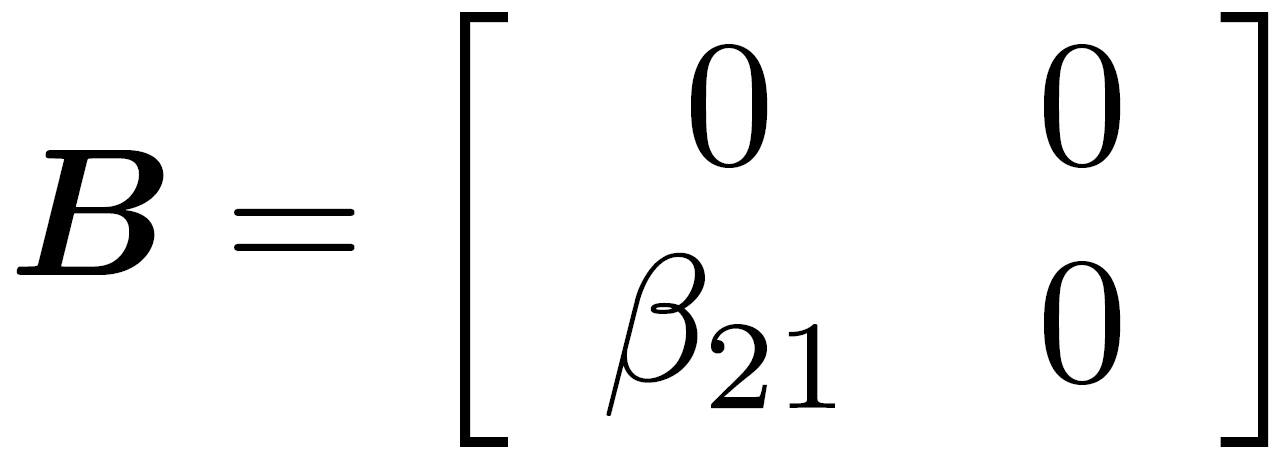

- \(B\) regression coefficients matrix \([m x m]\)

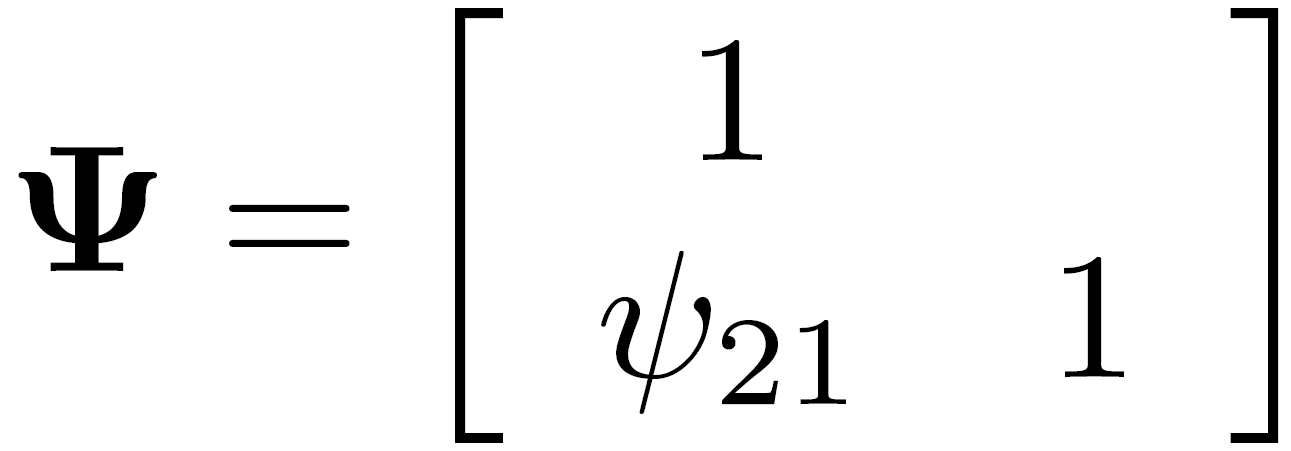

- \(\Psi\) residual structural errors covariance matrix \([m x m]\)

With p being the number of manifest variables and m being the number of latent variables.

The lavaan matrices

Lambda: matrix of loadings

Beta: regression coefficients

Psi: residual structural errors matrix

Theta: observed variance-covariance matrix

A SEM example - simulation

A SEM example - specification and constraints

Constraints

To estimate the model we need to set constraints:

- the

semorcfafunctions default is setting to 1 one loading for each latent variable - an alternative is to standardized latent variables using the

std.lv = TRUEoption

Constraints: default

[...]

Latent Variables:

Estimate Std.Err z-value P(>|z|) Std.lv Std.all

xi =~

x1 1.000 0.939 0.731

x2 0.558 0.221 2.529 0.011 0.524 0.445

eta =~

y1 1.000 0.538 0.458

y2 1.633 0.619 2.640 0.008 0.879 0.686

[...]

Variances:

Estimate Std.Err z-value P(>|z|) Std.lv Std.all

.x1 0.768 0.349 2.203 0.028 0.768 0.466

.x2 1.110 0.119 9.326 0.000 1.110 0.802

.y1 1.093 0.120 9.122 0.000 1.093 0.791

.y2 0.868 0.294 2.949 0.003 0.868 0.529

xi 0.882 0.353 2.497 0.013 1.000 1.000

.eta 0.272 0.106 2.564 0.010 0.941 0.941

[...]Constraints: std.lv=T

[...]

Latent Variables:

Estimate Std.Err z-value P(>|z|) Std.lv Std.all

xi =~

x1 0.939 0.188 4.994 0.000 0.939 0.731

x2 0.524 0.109 4.808 0.000 0.524 0.445

eta =~

y1 0.522 0.102 5.128 0.000 0.538 0.458

y2 0.853 0.171 4.997 0.000 0.879 0.686

[...]

Variances:

Estimate Std.Err z-value P(>|z|) Std.lv Std.all

.x1 0.768 0.349 2.203 0.028 0.768 0.466

.x2 1.110 0.119 9.326 0.000 1.110 0.802

.y1 1.093 0.120 9.122 0.000 1.093 0.791

.y2 0.868 0.294 2.949 0.003 0.868 0.529

xi 1.000 1.000 1.000

.eta 1.000 0.941 0.941

[...]lavaan matrices

$lambda

xi eta

x1 0.731 0.000

x2 0.445 0.000

y1 0.000 0.458

y2 0.000 0.686

$theta

x1 x2 y1 y2

x1 0.466

x2 0.000 0.802

y1 0.000 0.000 0.791

y2 0.000 0.000 0.000 0.529$psi

xi eta

xi 1.000

eta 0.000 0.941

$beta

xi eta

xi 0.000 0

eta 0.242 0SEM identification

Once again, remember that identification is a topic relevant to all structural equation models.

If an unknown parameter in \(\theta\) can be written as a function of one or more elements of \(\Sigma\), that parameter is identified.

If all unknown parameters in \(\theta\) are identified, the model is identified.

- the t-rule (again)

- the Two-Steps rule

Two-Steps rule

Step 1. Treat the model as a confirmatory factor analysis: view the original \(x\) and \(y\) as \(x\) variables and the original \(\xi\) and \(\eta\) as \(\xi\) variables. The only relationship between latent variables of interest are their variance and covariance \(Phi\). That is, ignore the \(B\), \(\Gamma\), and \(\Psi\) elements.

\(\rightarrow\) apply CFA identification rules

Step 2. Examine the latent variable equation of the original model (\(\eta = B\eta + \Gamma\xi + \zeta\)), assuming that each latent variable is an observed variable that is perfectly measured.

Two-Steps rule

Summary

If the first step shows that the measurement parameters are identified and the second step shows that the latent variable model parameters also are identified, then this is suficient to identify the whole model.

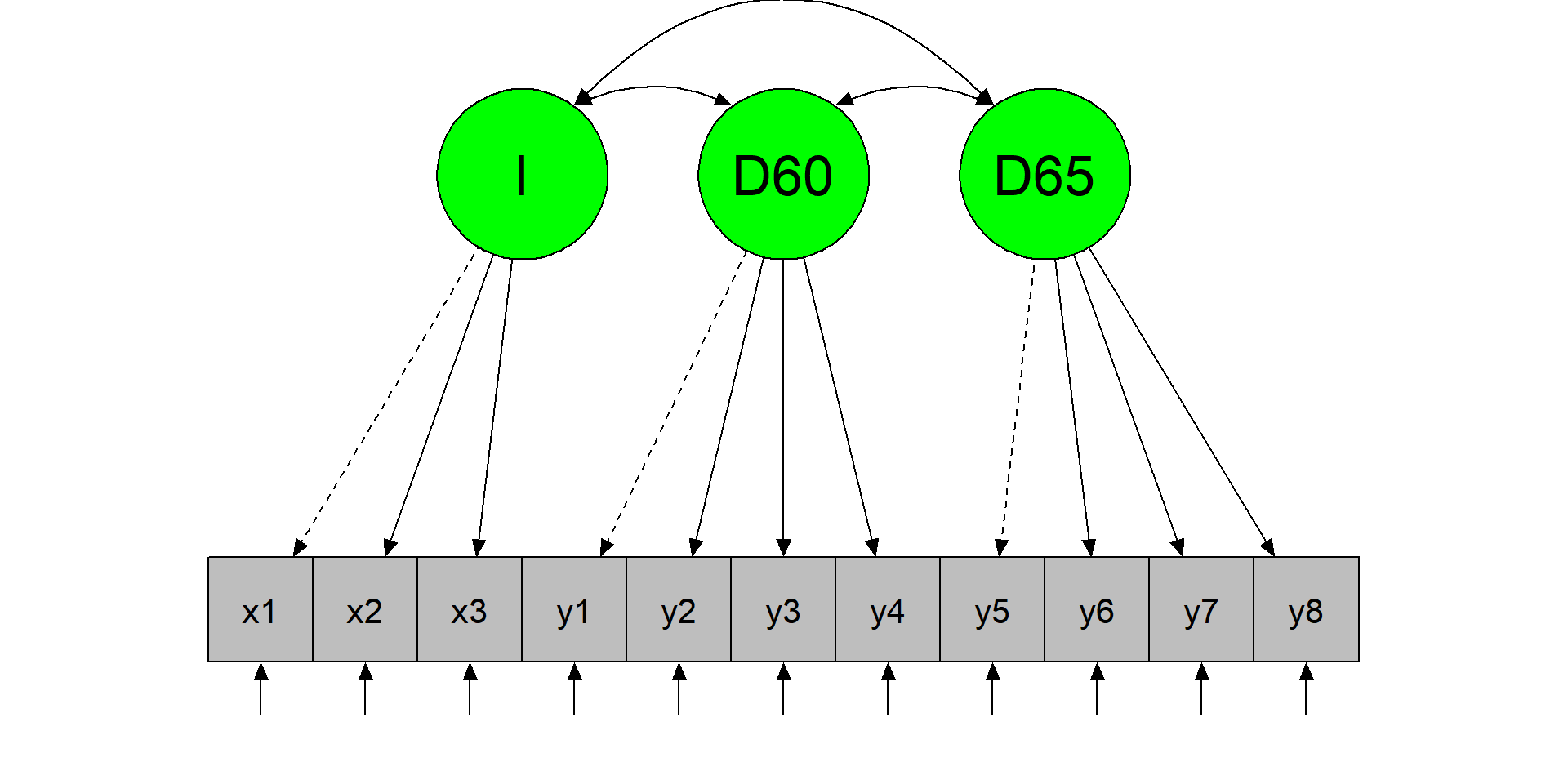

Political democracy dataset

Bollen (1989) studied the relation between industrialization in 1960 and political democracy of developing countries in 1960 and 1965.

We have 11 variables

y1 y2 y3 y4 y5 y6 y7 y8 x1 x2 x3

1 2.50 0.0 3.33 0.0 1.25 0.00 3.73 3.33 4.44 3.64 2.56

2 1.25 0.0 3.33 0.0 6.25 1.10 6.67 0.74 5.38 5.06 3.57

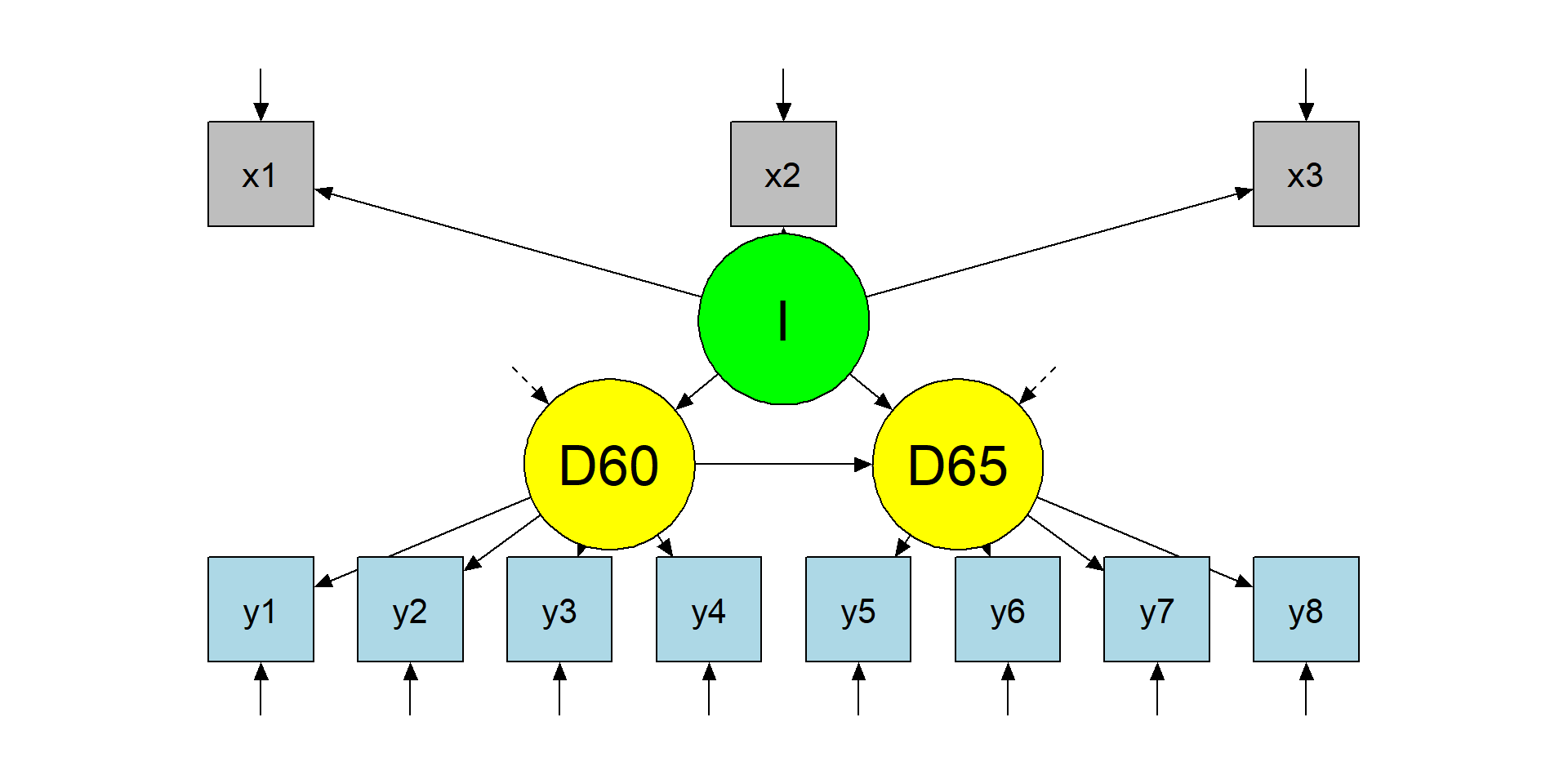

3 7.50 8.8 10.00 9.2 8.75 8.09 10.00 8.21 5.96 6.26 5.22A first latent variable, Industrialization (\(I = x_1 + x_2 + x_3\))

A second latent variable, political democracy in 1960 (\(D60 = y_1 + y_2 + y_3 + y_4\))

A third latent variable, political democracy in 1965 (\(D65 = y_5 + y_6 + y_7 + y_8\)).

LET'S APLLY THE TWO-STEPS RULE

Step 1 - model plot

The CFA model

Step 1 - model specification and results

The CFA model

PARAMETERS ARE ALL IDENTIFIED. LET'S GO TO STEP 2

Step 2 - model plot

The structural model

Step 2 - model specification and results

The structural model

STRUCTURAL PARAMETERS ARE ALSO IDENTIFIED.

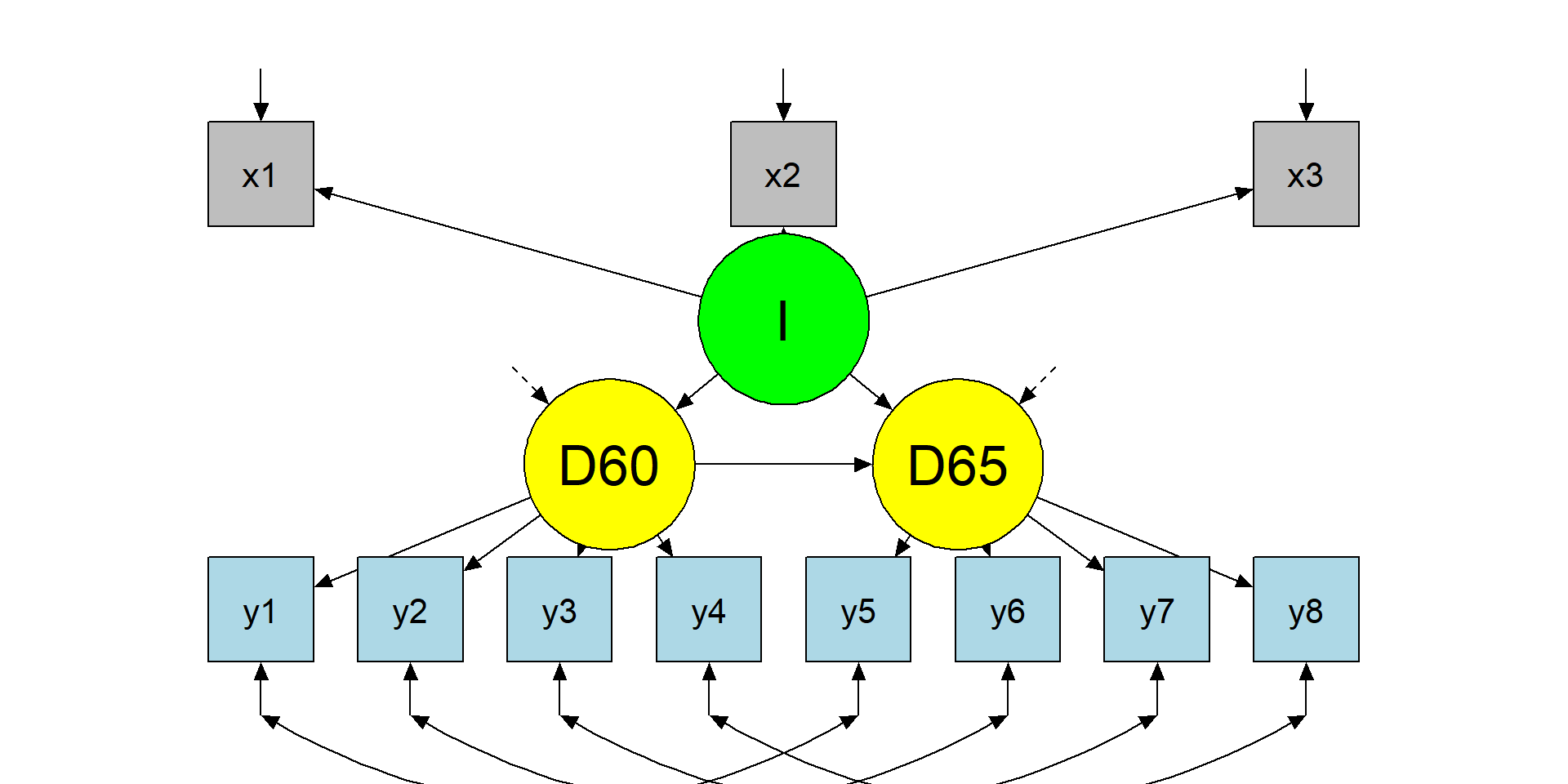

LET'S DEFINE THE MODEL CONSIDERING LONGITUDINAL MEASURES

Final model

The modified model

Final model specification

The modified model

SAME ITEMS AT DIFFERENT TIME POINTS HAVE CORRELATED RESIDUALS

Final model results

The modified model

lavaan 0.6-19 ended normally after 58 iterations

Estimator ML

Optimization method NLMINB

Number of model parameters 29

Number of observations 75

Model Test User Model:

Test statistic 50.835

Degrees of freedom 37

P-value (Chi-square) 0.064 cfi srmr rmsea

0.97952316 0.05011528 0.07060935 MODEL FIT IS GOOD!

Model comparisons

Warning: lavaan->lavTestLRT():

some models have the same degrees of freedom

Chi-Squared Difference Test

Df AIC BIC Chisq Chisq diff RMSEA Df diff Pr(>Chisq)

fit3 37 3166.3 3233.5 50.835

fit1 41 3179.9 3237.9 72.462 21.626 0.24239 4 0.0002378 ***

fit2 41 3179.9 3237.9 72.462 0.000 0.00000 0

---

Signif. codes: 0 '***' 0.001 '**' 0.01 '*' 0.05 '.' 0.1 ' ' 1Model comparisons

We can also compare the models using fit indices:

| chisq | df | cfi | tli | srmr | rmsea | aic | bic | |

|---|---|---|---|---|---|---|---|---|

| model1 | 72.462 | 41 | 0.953 | 0.938 | 0.055 | 0.101 | 3179.918 | 3237.855 |

| model2 | 72.462 | 41 | 0.953 | 0.938 | 0.055 | 0.101 | 3179.918 | 3237.855 |

| model3 | 50.835 | 37 | 0.980 | 0.970 | 0.050 | 0.071 | 3166.292 | 3233.499 |

WHAT IS THE BEST MODEL? QUESTIONS? COMMENTS?

Exercise

The EAT dataset

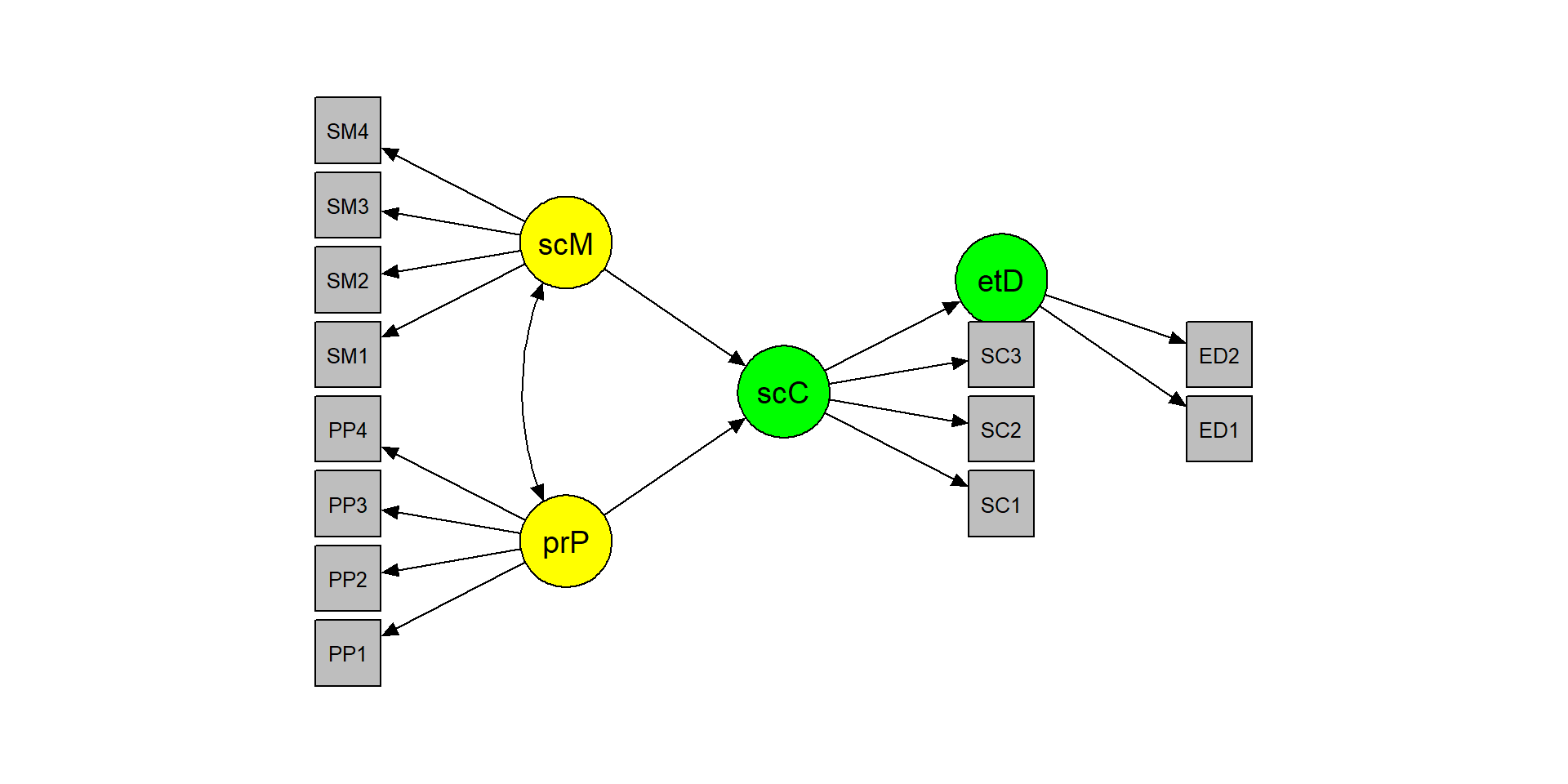

The dataset includes 13 items that measure ‘peer pressure’, ‘social media use’, ‘social comparison’, and ‘eating disorders’.

PP1 PP2 PP3 PP4 SM1 SM2 SM3 SM4 SC1 SC2 SC3 ED1 ED2

1 0.23 1.91 0.59 -0.70 2.31 1.06 1.43 -0.77 1.18 2.20 0.18 -0.38 1.61

2 -0.65 -3.18 -0.84 -0.43 0.69 0.10 1.24 0.51 -1.87 -1.17 -1.23 -1.74 -1.73

3 0.26 -1.46 -0.43 -0.05 -0.21 -0.46 -0.02 1.26 1.39 1.03 0.90 1.07 2.04

4 -0.68 -0.29 -0.08 -2.24 -0.64 0.47 -0.76 0.58 1.22 0.97 2.73 0.71 0.32

5 -0.06 0.89 0.04 -0.41 0.17 1.02 0.18 0.61 3.74 1.38 1.85 1.25 0.66

6 -0.29 -2.74 -0.52 2.58 0.15 -1.08 1.08 0.99 1.32 -0.24 0.93 -0.97 -0.68

The theoretical model

The exercise

- Apply the two-step rule:

- Test the CFA model

- Test the structural model

- Inspect model results and fit indices

- Are the hypotheses confirmed?

- Does the model fit the data well?

- If the model is not satisfactory, understand why and change it

- Draw the model (in

R, ppt, or with a pencil) - Try to fit a simple path model using sum scores instead of latent scores

Model specification

STEP 1 and 2

m1 <- "

# CFA model

peerPressure =~ PP1 + PP2 + PP3 + PP4

socialMedia =~ SM1 + SM2 + SM3 + SM4

socialComparison =~ SC1 + SC2 + SC3

eatingDisorder =~ ED1 + ED2

"

fit1 <- sem(m1, data = dE4_1, std.lv=T)

fit1@Fit@converged

m2 <- "

[...]

# Structural model

eatingDisorder ~ socialComparison

socialComparison ~ peerPressure + socialMedia"

fit2 <- sem(m2, data = dE4_1, std.lv=T)

fit2@Fit@convergedOK?

Results and fit

[...]

Regressions:

Estimate Std.Err z-value P(>|z|) Std.lv Std.all

eatingDisorder ~

socialComparsn 0.344 0.047 7.322 0.000 0.356 0.356

socialComparison ~

peerPressure 0.139 0.038 3.636 0.000 0.125 0.125

socialMedia 0.455 0.049 9.221 0.000 0.411 0.411

[...]Model modification

lhs op rhs mi epc sepc.lv sepc.all sepc.nox

120 SM1 ~~ SC2 328.967 0.565 0.565 0.628 0.628

49 socialMedia =~ SC2 56.910 0.378 0.378 0.289 0.289

57 socialComparison =~ SM1 54.668 0.292 0.323 0.283 0.283

121 SM1 ~~ SC3 51.713 -0.235 -0.235 -0.231 -0.231

50 socialMedia =~ SC3 30.539 -0.277 -0.277 -0.206 -0.206

119 SM1 ~~ SC1 22.069 -0.151 -0.151 -0.154 -0.154

143 SC1 ~~ SC3 19.170 0.293 0.293 0.285 0.285

74 PP1 ~~ PP2 18.341 0.665 0.665 1.201 1.201

97 PP3 ~~ PP4 15.333 0.126 0.126 0.109 0.109

58 socialComparison =~ SM2 13.081 -0.146 -0.162 -0.137 -0.137 cfi tli srmr rmsea

0.995 0.994 0.023 0.013 Why sum scores can mislead (measurement error → attenuation)

If an observed score \((X)\) is a noisy measure of a latent variable, measurement error tends to attenuate associations.

A classic intuition (simple linear setting):

\[ \hat\beta_{\text{observed}} \approx \hat\beta_{\text{latent}} \times \rho_{xx} \]

where \((\rho_{xx})\) is reliability of \((X)\).

This is exactly why latent-variable SEM can change “structural” conclusions even when factor scores correlate highly with sum scores.

Sum scores

d2 <- data.frame(

peerPressure = dE4_1$PP1 + dE4_1$PP2 + dE4_1$PP3 + dE4_1$PP4,

socialMedia = dE4_1$SM1 + dE4_1$SM2 + dE4_1$SM3 + dE4_1$SM4,

socialComparison = dE4_1$SC1 + dE4_1$SC2 + dE4_1$SC3,

eatingDisorder = dE4_1$ED1 + dE4_1$ED2)

path <- "

eatingDisorder ~ socialComparison

socialComparison ~ peerPressure + socialMedia"

fitP <- sem(path, d2)

fitmeasures(fitP, fit.measures =

c("cfi", "tli", "srmr", "rmsea")) cfi tli srmr rmsea

0.978 0.946 0.019 0.037 The ground truth

# peer pressure AND social media -> social comparison -> eating disorder

mE4_1 <- "

# CFA model

peerPressure =~ .75*PP1 + .72*PP2 + .59*PP3 + .65*PP4

socialMedia =~ .45*SM1 + .55*SM2 + .59*SM3 + .65*SM4

socialComparison =~ .81*SC1 + .75*SC2 + .86*SC3

eatingDisorder =~ .70*ED1 + .65*ED2

# Structural model

eatingDisorder ~ .37*socialComparison

socialComparison ~ .23*peerPressure + .41*socialMedia

# Misspecifications

# within construct

PP1 ~~ .43*PP2

# between construct

SM1 ~~ .53*SC2

"Sum scores VS latent scores

However, the debate is still open:

Thinking twice about sum scores (McNeish & Wolf, 2020)

Thinking thrice about sum scores, and then some more about measurement and analysis (Widaman & Revelle, 2022)

Psychometric properties of sum scores and factor scores differ even when their correlation is 0.98: A response to Widaman and Revelle (McNeish, 2023)

Thinking About Sum Scores Yet Again, Maybe the Last Time, We Don’t Know, Oh No (Widaman & Revelle, 2024)

Or some more Schimmack:

- Schimmack vs Gelman 1 (https://replicationindex.com/2023/11/17/loken-and-gelman-are-still-wrong/)

- Schimmack vs Gelman 2 (https://replicationindex.com/2023/11/25/loken-and-gelmans-simulation-is-not-a-fair-comparison/)

Indicator indifference: a measurement question with structural consequences

- How much should our conclusions depend on the specific items we happened to include?

- How many indicators are enough to recover a latent relation with reasonable precision?

- Is it better to have more indicators, or fewer but stronger and more central indicators?

- What happens when indicators differ in loading strength, construct centrality, or contamination?

- If the structural path changes a lot when we swap reasonable indicators, are we estimating a robust latent relation — or an item-bound result?

See the extra module

Exercises (Lab 05)

Go to:

labs/labs/lab05_sem_capstone_eat.qmdlink

You will practice:

- Apply the Two-Step rule (identify/fit measurement first, then structure)

- Evaluate the model using fit indices + diagnostics (global + local)

- Use MI + EPC/SEPC to propose a theory-justified modification

- Compare a latent SEM vs a sum-score path model

Take-home: 3 things

- SEM is measurement + structure — structural paths do not rescue poor measurement

- Treat fit indices and diagnostics as routine checks (global + local), not as a one-time hurdle

- Comparing models is scientific: theory → constraints → estimation → evaluation → transparent revision

Acknowledgments

Thanks to Massimiliano Pastore for his slides!

References

McNeish, D. (2023). Psychometric properties of sum scores and factor scores differ even when their correlation is 0.98: A response to Widaman and Revelle. Behavior Research Methods, 55(8), 4269–4290. https://doi.org/10.3758/s13428-022-02016-x

McNeish, D., & Wolf, M. G. (2020). Thinking twice about sum scores. Behavior Research Methods, 52(6), 2287–2305. https://doi.org/10.3758/s13428-020-01398-0

Widaman, K. F., & Revelle, W. (2022). Thinking thrice about sum scores, and then some more about measurement and analysis. Behavior Research Methods. https://doi.org/10.3758/s13428-022-01849-w

Widaman, K. F., & Revelle, W. (2024). Thinking About Sum Scores Yet Again, Maybe the Last Time, We Don’t Know, Oh No . . .1: A Comment on McNeish (2023). Educational and Psychological Measurement, 84(4), 637–659. https://doi.org/10.1177/00131644231205310